82:. Naked option are attractive because the seller receives the premium cost of the option without buying a corresponding position to hedge against potential losses. In the case of a naked put, the seller hopes that the underlying equity or stock price stays the same or rises. In the case of a naked call, the seller hopes that the underlying equity or stock price stays the same or drops. And the seller's odds of retaining the premium at expiration increase the further the naked option is

28:

20:

1198:

106:

However, the naked option has the highest risk because sellers have agreed to cover the contract in case of assignment, no matter how far the price of the stock goes. The seller of a naked put would be obligated to purchase the underlying stock at the strike price even if its market price drops down

124:

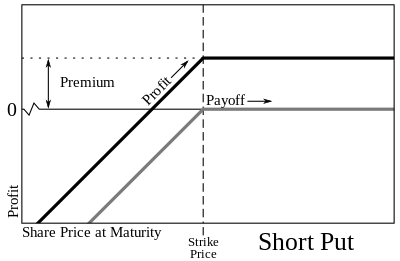

Shares of XYZ is currently selling at $ 85 per share and

Speculator A decides to sell a call option at a strike price of $ 100 per share on or before May 10 for $ 24. If the XYZ shares fail to rise above $ 100 before May 10, the call option expires worthless and Speculator A makes a profit of $ 24.

138:

Shares of XYZ is currently selling at $ 85 per share and

Speculator A decides to sell a put option at a strike price of $ 75 per share on or before June 10 for $ 24. If the XYZ shares fail to drop below $ 75 before June 10, the put option expires worthless and Speculator A makes a profit of $ 24.

129:

and sell them back for $ 100 each. In this scenario, the

Speculator A makes a loss of (100 * XYZ market price) - (100 * $ 100) - $ 24. As market price can rise an unlimited amount, Speculator A can experience unlimited losses in this 'worst case' scenario.

107:

to zero. Likewise, the seller of a naked call could be forced to short the underlying stock at the strike price even if its market price rises up to an unlimited amount. Because nothing is covered to protect against potential losses, a

102:

at assignment or expiration. Likewise, one with sufficient equity to borrow on margin could sell a call option, receive the premium, and then short the stock if its price rises to or above the strike price at assignment or expiration.

97:

to open an equity position. Instead of buying an underlying stock outright, one with sufficient cash could sell a put option, receive the premium, and then buy the stock if its price drops to or below the

139:

However, if the XYZ shares drop at or below $ 75, Speculator A would be obligated to buy 100 shares of XYZ at a price of $ 75, even if the market price drops at or near $ 0.

741:

316:

1081:

771:

59:). Nor does the seller hold any option of the same class on the same underlying asset that could protect against potential losses (like in an

268:

Mark D. Wolfinger, "The Rookie's Guide to

Options" The Beginner's Handbook of Trading Equity Options" W&A Publishing, Cedar Falls, 2008.

903:

247:

639:

1141:

309:

1076:

721:

78:, and therefore most brokers restrict them to only those traders that have the highest options level approval and have a

1116:

654:

508:

302:

735:

1223:

913:

111:

would be triggered if the seller does not have enough equity or cash to cover the contract in case of assignment.

1017:

828:

1136:

1131:

786:

731:

1086:

756:

746:

614:

455:

387:

190:

1035:

883:

868:

833:

776:

125:

However, if the XYZ shares rise above $ 100, Speculator A would be obligated to buy 100 shares of XYZ at

1096:

947:

863:

440:

761:

1050:

1007:

997:

987:

708:

649:

584:

538:

533:

407:

367:

334:

766:

1055:

843:

589:

1106:

1091:

1060:

1045:

1012:

878:

669:

634:

397:

362:

325:

221:

75:

1111:

1101:

1040:

1027:

1002:

888:

674:

470:

251:

992:

982:

972:

931:

926:

908:

838:

604:

599:

571:

523:

402:

342:

79:

48:

44:

1202:

1172:

1167:

1121:

957:

952:

898:

808:

716:

689:

629:

624:

594:

543:

528:

445:

425:

1177:

1162:

962:

873:

823:

800:

781:

609:

551:

518:

513:

493:

417:

157:

60:

56:

1217:

1157:

1126:

967:

893:

853:

848:

684:

556:

503:

498:

480:

377:

357:

977:

751:

679:

619:

488:

460:

450:

392:

283:

99:

288:

858:

726:

697:

693:

644:

435:

430:

126:

108:

90:

64:

27:

19:

1182:

818:

813:

579:

465:

94:

68:

372:

83:

1197:

942:

664:

561:

382:

222:"What to know about naked options — from how it works to why it's risky"

89:

Selling a naked option could also be used as an alternative to using a

67:" is called a "naked call" or "uncovered call", while one involving a "

294:

52:

26:

18:

298:

278:

55:

to cover the contract in case of assignment (like in a

51:

writer (i.e., the seller) does not hold the underlying

1150:

1069:

1026:

922:

799:

707:

570:

479:

416:

350:

341:

310:

8:

347:

317:

303:

295:

215:

213:

211:

184:

182:

180:

178:

1142:Power reverse dual-currency note (PRDC)

1082:Constant proportion portfolio insurance

148:

71:" is a "naked put" or "uncovered put".

7:

1077:Collateralized debt obligation (CDO)

74:The naked option is one of riskiest

156:Scott, Gordon (December 31, 2021).

191:"Naked Options Expose You to Risk"

31:Payoffs from a short call position

14:

248:"When to Use A Naked Call Option"

220:Chandler, Simon (July 29, 2022).

23:Payoffs from a short put position

1196:

63:). A naked option involving a "

904:Year-on-year inflation-indexed

279:Chicago Board Options Exchange

189:Butler, Chad (July 11, 2022).

1:

914:Zero-coupon inflation-indexed

246:Juggernaut (July 12, 2012).

86:at the time it was written.

1117:Foreign exchange derivative

509:Callable bull/bear contract

1240:

1191:

1018:Stock market index future

332:

284:Australian Stock Exchange

1137:Mortgage-backed security

1132:Interest rate derivative

1107:Equity-linked note (ELN)

1092:Credit-linked note (CLN)

1087:Contract for difference

388:Risk-free interest rate

869:Forward Rate Agreement

32:

24:

1097:Credit default option

441:Employee stock option

30:

22:

1051:Inflation derivative

1036:Commodity derivative

1008:Single-stock futures

998:Normal backwardation

988:Interest rate future

829:Conditional variance

335:Derivative (finance)

1203:Business portal

1056:Property derivative

16:Investment strategy

1061:Weather derivative

1046:Freight derivative

1028:Exotic derivatives

948:Commodities future

635:Intermarket spread

398:Synthetic position

326:Derivatives market

291:, Options tutorial

120:Naked call example

76:options strategies

33:

25:

1224:Options (finance)

1211:

1210:

1112:Equity derivative

1102:Credit derivative

1070:Other derivatives

1041:Energy derivative

1003:Perpetual futures

884:Overnight indexed

834:Constant maturity

795:

794:

742:Finite difference

675:Protective option

254:on July 10, 2013.

134:Naked put example

1231:

1201:

1200:

973:Forwards pricing

747:Garman–Kohlhagen

348:

319:

312:

305:

296:

256:

255:

250:. Archived from

243:

237:

236:

234:

232:

226:Business Insider

217:

206:

205:

203:

201:

186:

173:

172:

170:

168:

153:

84:out of the money

49:options contract

45:options strategy

41:uncovered option

1239:

1238:

1234:

1233:

1232:

1230:

1229:

1228:

1214:

1213:

1212:

1207:

1195:

1187:

1173:Great Recession

1168:Government debt

1146:

1122:Fund derivative

1065:

1022:

983:Futures pricing

958:Dividend future

953:Currency future

936:

918:

791:

767:Put–call parity

703:

690:Vertical spread

625:Diagonal spread

595:Calendar spread

566:

475:

412:

337:

328:

323:

275:

265:

263:Further reading

260:

259:

245:

244:

240:

230:

228:

219:

218:

209:

199:

197:

188:

187:

176:

166:

164:

155:

154:

150:

145:

136:

122:

117:

17:

12:

11:

5:

1237:

1235:

1227:

1226:

1216:

1215:

1209:

1208:

1206:

1205:

1192:

1189:

1188:

1186:

1185:

1180:

1178:Municipal debt

1175:

1170:

1165:

1163:Corporate debt

1160:

1154:

1152:

1148:

1147:

1145:

1144:

1139:

1134:

1129:

1124:

1119:

1114:

1109:

1104:

1099:

1094:

1089:

1084:

1079:

1073:

1071:

1067:

1066:

1064:

1063:

1058:

1053:

1048:

1043:

1038:

1032:

1030:

1024:

1023:

1021:

1020:

1015:

1010:

1005:

1000:

995:

990:

985:

980:

975:

970:

965:

963:Forward market

960:

955:

950:

945:

939:

937:

935:

934:

929:

923:

920:

919:

917:

916:

911:

906:

901:

896:

891:

886:

881:

876:

871:

866:

861:

856:

851:

846:

844:Credit default

841:

836:

831:

826:

821:

816:

811:

805:

803:

797:

796:

793:

792:

790:

789:

784:

779:

774:

769:

764:

759:

754:

749:

744:

739:

729:

724:

719:

713:

711:

705:

704:

702:

701:

687:

682:

677:

672:

667:

662:

657:

652:

647:

642:

640:Iron butterfly

637:

632:

627:

622:

617:

612:

610:Covered option

607:

602:

597:

592:

587:

582:

576:

574:

568:

567:

565:

564:

559:

554:

549:

548:Mountain range

546:

541:

536:

531:

526:

521:

516:

511:

506:

501:

496:

491:

485:

483:

477:

476:

474:

473:

468:

463:

458:

453:

448:

443:

438:

433:

428:

422:

420:

414:

413:

411:

410:

405:

400:

395:

390:

385:

380:

375:

370:

365:

360:

354:

352:

345:

339:

338:

333:

330:

329:

324:

322:

321:

314:

307:

299:

293:

292:

286:

281:

274:

273:External links

271:

270:

269:

264:

261:

258:

257:

238:

207:

174:

158:"Naked Option"

147:

146:

144:

141:

135:

132:

121:

118:

116:

113:

80:margin account

61:options spread

57:covered option

15:

13:

10:

9:

6:

4:

3:

2:

1236:

1225:

1222:

1221:

1219:

1204:

1199:

1194:

1193:

1190:

1184:

1181:

1179:

1176:

1174:

1171:

1169:

1166:

1164:

1161:

1159:

1158:Consumer debt

1156:

1155:

1153:

1151:Market issues

1149:

1143:

1140:

1138:

1135:

1133:

1130:

1128:

1127:Fund of funds

1125:

1123:

1120:

1118:

1115:

1113:

1110:

1108:

1105:

1103:

1100:

1098:

1095:

1093:

1090:

1088:

1085:

1083:

1080:

1078:

1075:

1074:

1072:

1068:

1062:

1059:

1057:

1054:

1052:

1049:

1047:

1044:

1042:

1039:

1037:

1034:

1033:

1031:

1029:

1025:

1019:

1016:

1014:

1011:

1009:

1006:

1004:

1001:

999:

996:

994:

991:

989:

986:

984:

981:

979:

976:

974:

971:

969:

968:Forward price

966:

964:

961:

959:

956:

954:

951:

949:

946:

944:

941:

940:

938:

933:

930:

928:

925:

924:

921:

915:

912:

910:

907:

905:

902:

900:

897:

895:

892:

890:

887:

885:

882:

880:

879:Interest rate

877:

875:

872:

870:

867:

865:

862:

860:

857:

855:

852:

850:

847:

845:

842:

840:

837:

835:

832:

830:

827:

825:

822:

820:

817:

815:

812:

810:

807:

806:

804:

802:

798:

788:

785:

783:

780:

778:

775:

773:

772:MC Simulation

770:

768:

765:

763:

760:

758:

755:

753:

750:

748:

745:

743:

740:

737:

733:

732:Black–Scholes

730:

728:

725:

723:

720:

718:

715:

714:

712:

710:

706:

699:

695:

691:

688:

686:

685:Risk reversal

683:

681:

678:

676:

673:

671:

668:

666:

663:

661:

658:

656:

653:

651:

648:

646:

643:

641:

638:

636:

633:

631:

628:

626:

623:

621:

618:

616:

615:Credit spread

613:

611:

608:

606:

603:

601:

598:

596:

593:

591:

588:

586:

583:

581:

578:

577:

575:

573:

569:

563:

560:

558:

555:

553:

550:

547:

545:

542:

540:

539:Interest rate

537:

535:

534:Forward start

532:

530:

527:

525:

522:

520:

517:

515:

512:

510:

507:

505:

502:

500:

497:

495:

492:

490:

487:

486:

484:

482:

478:

472:

469:

467:

464:

462:

461:Option styles

459:

457:

454:

452:

449:

447:

444:

442:

439:

437:

434:

432:

429:

427:

424:

423:

421:

419:

415:

409:

406:

404:

401:

399:

396:

394:

391:

389:

386:

384:

381:

379:

378:Open interest

376:

374:

371:

369:

366:

364:

361:

359:

358:Delta neutral

356:

355:

353:

349:

346:

344:

340:

336:

331:

327:

320:

315:

313:

308:

306:

301:

300:

297:

290:

287:

285:

282:

280:

277:

276:

272:

267:

266:

262:

253:

249:

242:

239:

227:

223:

216:

214:

212:

208:

196:

192:

185:

183:

181:

179:

175:

163:

159:

152:

149:

142:

140:

133:

131:

128:

119:

114:

112:

110:

104:

101:

96:

92:

87:

85:

81:

77:

72:

70:

66:

62:

58:

54:

50:

46:

42:

38:

29:

21:

978:Forward rate

889:Total return

777:Real options

680:Ratio spread

660:Naked option

659:

620:Debit spread

451:Fixed income

393:Strike price

289:Investopedia

252:the original

241:

229:. Retrieved

225:

198:. Retrieved

195:Investopedia

194:

165:. Retrieved

162:Investopedia

161:

151:

137:

127:market price

123:

105:

100:strike price

88:

73:

40:

37:naked option

36:

34:

909:Zero Coupon

839:Correlation

787:Vanna–Volga

645:Iron condor

431:Bond option

109:margin call

91:limit order

1183:Tax policy

899:Volatility

809:Amortising

650:Jelly roll

585:Box spread

580:Backspread

572:Strategies

408:Volatility

403:the Greeks

368:Expiration

231:October 1,

200:October 1,

167:October 1,

143:References

95:stop order

47:where the

874:Inflation

824:Commodity

782:Trinomial

717:Bachelier

709:Valuation

590:Butterfly

524:Commodore

373:Moneyness

1218:Category

1013:Slippage

943:Contango

927:Forwards

894:Variance

854:Dividend

849:Currency

762:Margrabe

757:Lattices

736:equation

722:Binomial

670:Strangle

665:Straddle

562:Swaption

544:Lookback

529:Compound

471:Warrants

446:European

426:American

418:Vanillas

383:Pin risk

363:Exercise

115:Examples

932:Futures

552:Rainbow

519:Cliquet

514:Chooser

494:Barrier

481:Exotics

343:Options

993:Margin

859:Equity

752:Heston

655:Ladder

605:Condor

600:Collar

557:Spread

504:Binary

499:Basket

43:is an

864:Forex

819:Basis

814:Asset

801:Swaps

727:Black

630:Fence

489:Asian

351:Terms

53:asset

698:Bull

694:Bear

436:Call

233:2022

202:2022

169:2022

65:call

466:Put

93:or

69:put

39:or

1220::

696:,

456:FX

224:.

210:^

193:.

177:^

160:.

35:A

738:)

734:(

700:)

692:(

318:e

311:t

304:v

235:.

204:.

171:.

Text is available under the Creative Commons Attribution-ShareAlike License. Additional terms may apply.