133:

36:

683:

219:

Low average propensity to save might be the indicator of a large percentage of old people or high percentage of irresponsible young people in the population. With income level changes, APS becomes an inexact tool for measuring these changes. So, the marginal propensity to save is used in these cases.

212:(as expectations of rising prices can encourage people to spend now rather than later) or current interest rates. APS can express the social preference for investing in the future over consuming in the present. The complement (1 minus the APS) is the

132:

207:

The ratio differs considerably over time and between countries. The savings ratio for an entire economy can be affected by (for example) the proportion of older people (as they have less motivation and capability to save), and the rate of

567:

508:

308:

203:

329:

As is a fraction of income, an increase in income would make the proportion of saving lower. Also income rises faster than savings so APS tens to decrease as income increase.

365:

613:

590:

265:

452:

432:

412:

392:

53:

318:

Average propensity to save can not be greater than or equal to 1, but APS can be negative, if income is zero and consumption has a positive value.

758:

100:

724:

72:

645:

119:

519:

312:

APS can be calculated as total savings divided by the income level for which we want to determine the average propensity to save.

79:

743:

635:

57:

86:

625:

213:

68:

630:

460:

46:

753:

748:

640:

337:

Marginal propensity to save is the proportion of an increase in income devoted to savings. Mathematically, the

315:

Example 1: The income level is 90 and total savings for that level is 25, then we will get 25/90 as the APS.

717:

274:

169:

93:

665:

372:

340:

141:

710:

595:

572:

161:

694:

238:

437:

417:

397:

377:

737:

321:

Example 2: The income is 0 and consumption is 20, so the APS value will be -0.2.

35:

368:

17:

690:

209:

682:

157:

269:

APS is calculated from the amount of savings as a fraction of income.

153:

666:

https://www.investopedia.com/terms/a/average-propensity-to-save.asp

131:

615:

is the change in disposable income that produced the consumption.

29:

562:{\displaystyle {\mathit {MPS}}={\frac {\Delta S}{\Delta Y}}}

531:

528:

525:

472:

469:

466:

352:

349:

346:

698:

598:

575:

522:

463:

440:

420:

400:

380:

343:

277:

241:

172:

136:

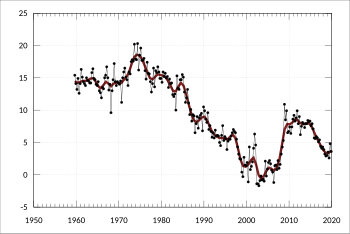

The household savings ratio in

Australia since 1959

60:. Unsourced material may be challenged and removed.

607:

584:

561:

502:

446:

426:

406:

386:

359:

302:

259:

197:

503:{\displaystyle {\mathit {MPS}}={\frac {dS}{dY}}}

156:which is saved, usually expressed for household

718:

8:

725:

711:

597:

574:

539:

524:

523:

521:

480:

465:

464:

462:

439:

419:

399:

379:

345:

344:

342:

290:

276:

240:

185:

171:

120:Learn how and when to remove this message

325:Average propensity to save is decreasing

657:

414:, i.e., the instantaneous slope of the

7:

679:

677:

58:adding citations to reliable sources

27:Proportion of income which is saved

697:. You can help Knowledge (XXG) by

646:Kinetic exchange models of markets

599:

576:

550:

542:

394:with respect to disposable income

303:{\displaystyle APS={\frac {S}{Y}}}

198:{\displaystyle APS={\frac {S}{Y}}}

25:

333:Marginal propensity to save (MPS)

160:as a fraction of total household

681:

146:average propensity to save (APS)

34:

360:{\displaystyle {\mathit {MPS}}}

45:needs additional citations for

636:Marginal propensity to consume

592:is the change in savings, and

1:

626:Average propensity to consume

367:function is expressed as the

214:average propensity to consume

664:Average Propensity To Save,

69:"Average propensity to save"

759:Economics and finance stubs

631:Marginal propensity to save

775:

676:

641:Golden Rule savings rate

608:{\displaystyle \Delta Y}

585:{\displaystyle \Delta S}

152:, is the proportion of

744:Gross domestic product

693:-related article is a

609:

586:

563:

504:

448:

428:

408:

388:

361:

304:

261:

224:Characteristics of APS

199:

137:

610:

587:

564:

505:

449:

429:

409:

389:

362:

305:

262:

260:{\displaystyle Y=C+S}

200:

135:

596:

573:

520:

461:

438:

418:

398:

378:

341:

275:

239:

170:

148:, also known as the

54:improve this article

513:or, approximately,

233:From the equation:

142:Keynesian economics

605:

582:

559:

500:

444:

424:

404:

384:

357:

300:

257:

195:

138:

706:

705:

557:

498:

447:{\displaystyle Y}

427:{\displaystyle S}

407:{\displaystyle Y}

387:{\displaystyle S}

298:

193:

164:(taxed income).

162:disposable income

130:

129:

122:

104:

16:(Redirected from

766:

754:Financial ratios

749:Personal finance

727:

720:

713:

685:

678:

668:

662:

614:

612:

611:

606:

591:

589:

588:

583:

568:

566:

565:

560:

558:

556:

548:

540:

535:

534:

509:

507:

506:

501:

499:

497:

489:

481:

476:

475:

453:

451:

450:

445:

433:

431:

430:

425:

413:

411:

410:

405:

393:

391:

390:

385:

373:savings function

366:

364:

363:

358:

356:

355:

309:

307:

306:

301:

299:

291:

266:

264:

263:

258:

204:

202:

201:

196:

194:

186:

125:

118:

114:

111:

105:

103:

62:

38:

30:

21:

774:

773:

769:

768:

767:

765:

764:

763:

734:

733:

732:

731:

674:

672:

671:

663:

659:

654:

622:

594:

593:

571:

570:

549:

541:

518:

517:

490:

482:

459:

458:

436:

435:

416:

415:

396:

395:

376:

375:

339:

338:

335:

327:

273:

272:

237:

236:

231:

226:

168:

167:

126:

115:

109:

106:

63:

61:

51:

39:

28:

23:

22:

15:

12:

11:

5:

772:

770:

762:

761:

756:

751:

746:

736:

735:

730:

729:

722:

715:

707:

704:

703:

686:

670:

669:

656:

655:

653:

650:

649:

648:

643:

638:

633:

628:

621:

618:

617:

616:

604:

601:

581:

578:

555:

552:

547:

544:

538:

533:

530:

527:

511:

510:

496:

493:

488:

485:

479:

474:

471:

468:

443:

423:

403:

383:

354:

351:

348:

334:

331:

326:

323:

297:

294:

289:

286:

283:

280:

256:

253:

250:

247:

244:

230:

227:

225:

222:

192:

189:

184:

181:

178:

175:

128:

127:

42:

40:

33:

26:

24:

14:

13:

10:

9:

6:

4:

3:

2:

771:

760:

757:

755:

752:

750:

747:

745:

742:

741:

739:

728:

723:

721:

716:

714:

709:

708:

702:

700:

696:

692:

687:

684:

680:

675:

667:

661:

658:

651:

647:

644:

642:

639:

637:

634:

632:

629:

627:

624:

623:

619:

602:

579:

553:

545:

536:

516:

515:

514:

494:

491:

486:

483:

477:

457:

456:

455:

441:

421:

401:

381:

374:

370:

332:

330:

324:

322:

319:

316:

313:

310:

295:

292:

287:

284:

281:

278:

270:

267:

254:

251:

248:

245:

242:

234:

228:

223:

221:

217:

215:

211:

205:

190:

187:

182:

179:

176:

173:

165:

163:

159:

155:

151:

150:savings ratio

147:

143:

134:

124:

121:

113:

110:December 2018

102:

99:

95:

92:

88:

85:

81:

78:

74:

71: –

70:

66:

65:Find sources:

59:

55:

49:

48:

43:This article

41:

37:

32:

31:

19:

18:Savings ratio

699:expanding it

688:

673:

660:

512:

336:

328:

320:

317:

314:

311:

271:

268:

235:

232:

218:

206:

166:

149:

145:

139:

116:

107:

97:

90:

83:

76:

64:

52:Please help

47:verification

44:

229:Mathematics

738:Categories

652:References

369:derivative

80:newspapers

691:economics

600:Δ

577:Δ

551:Δ

543:Δ

210:inflation

620:See also

569:, where

454:curve.

371:of the

216:(APC).

158:savings

94:scholar

154:income

144:, the

96:

89:

82:

75:

67:

689:This

101:JSTOR

87:books

695:stub

73:news

140:In

56:by

740::

726:e

719:t

712:v

701:.

603:Y

580:S

554:Y

546:S

537:=

532:S

529:P

526:M

495:Y

492:d

487:S

484:d

478:=

473:S

470:P

467:M

442:Y

434:-

422:S

402:Y

382:S

353:S

350:P

347:M

296:Y

293:S

288:=

285:S

282:P

279:A

255:S

252:+

249:C

246:=

243:Y

191:Y

188:S

183:=

180:S

177:P

174:A

123:)

117:(

112:)

108:(

98:·

91:·

84:·

77:·

50:.

20:)

Text is available under the Creative Commons Attribution-ShareAlike License. Additional terms may apply.