738:

730:

22:

839:

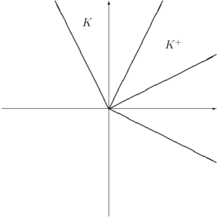

Assume further that there is 50% transaction costs for each deal. This means that (1A,-1M) and (-1A,1M) cannot be exchanged into non-negative portfolios. But, (2A,-1M) and (-1A,2M) can be traded into non-negative portfolios. It can be seen that

715:

939:

1131:

1021:

209:

829:

602:

427:

530:

305:

490:

1231:

1054:

350:

40:

235:

1157:

120:

261:

1185:

455:

140:

625:

717:) are the set of prices which would define a friction-less pricing system for the assets that is consistent with the market. This is also called a

1258:

Schachermayer, Walter (November 15, 2002). "The

Fundamental Theorem of Asset Pricing under Proportional Transaction Costs in Finite Discrete Time".

611:

The negative of a solvency cone is the set of portfolios that can be obtained starting from the zero portfolio. This is intimately related to

843:

1061:

951:

944:

The dual cone of prices is thus easiest to see in terms of prices of A in terms of M (and similarly done for price of M in terms of A):

58:

145:

1386:

760:

543:

355:

91:

of portfolios that can be exchanged to portfolios of non-negative components (including paying of any transaction costs).

495:

266:

718:

460:

612:

1196:

1299:

1026:

310:

1263:

76:

237:

is the number of assets which with any non-negative quantity of them can be "discarded" (traditionally

737:

1304:

754:

729:

1362:

1336:

80:

1354:

84:

214:

1346:

1309:

1136:

1276:

105:

240:

1170:

440:

125:

100:

757:, we can obviously make (1A,-1M) and (-1A,1M) into non-negative portfolios, therefore

710:{\displaystyle K^{+}=\left\{w\in \mathbb {R} ^{d}:\forall v\in K:0\leq w^{T}v\right\}}

1380:

1366:

88:

1350:

1191:

contains a line, then there is an exchange possible without transaction costs.

1358:

1327:

Löhne, Andreas; Rudloff, Birgit (2015). "On the dual of the solvency cone".

619:

1290:

Hamel, A. H.; Heyde, F. (2010). "Duality for Set-Valued

Measures of Risk".

1234:

1313:

934:{\displaystyle K=\{x\in \mathbb {R} ^{2}:(2,1)x\geq 0,(1,2)x\geq 0\}}

1233:, then there is no possible exchange, i.e. the market is completely

1126:{\displaystyle (1,0)\rightarrow (0,t)\rightarrow ({\frac {t}{2}},0)}

1016:{\displaystyle (0,t)\rightarrow (1,0)\rightarrow (0,{\frac {1}{2}})}

1341:

745:

Assume there are 2 assets, A and M with 1 to 1 exchange possible.

736:

728:

604:

is a model of a financial market. This is sometimes called a

15:

204:{\displaystyle \Pi =\left(\pi ^{ij}\right)_{1\leq i,j\leq d}}

824:{\displaystyle K=\{x\in \mathbb {R} ^{2}:(1,1)x\geq 0\}}

597:{\displaystyle \left\{K_{t}(\omega )\right\}_{t=0}^{T}}

36:

1199:

1173:

1139:

1064:

1029:

954:

846:

763:

628:

546:

498:

463:

443:

358:

313:

269:

243:

217:

148:

128:

108:

422:{\displaystyle \pi ^{ij}e^{i}-e^{j},1\leq i,j\leq d}

31:

may be too technical for most readers to understand

1225:

1179:

1151:

1125:

1048:

1015:

933:

823:

709:

596:

524:

484:

449:

421:

344:

299:

255:

229:

203:

134:

114:

83:. This is of particular interest to markets with

525:{\displaystyle K\supseteq \mathbb {R} _{+}^{d}}

307:is the convex cone spanned by the unit vectors

300:{\displaystyle K(\Pi )\subset \mathbb {R} ^{d}}

733:Sample solvency cone with no transaction costs

8:

928:

853:

818:

770:

741:Sample solvency cone with transaction costs

485:{\displaystyle K\subseteq \mathbb {R} ^{d}}

831:. Note that (1,1) is the "price vector."

1340:

1303:

1217:

1212:

1208:

1207:

1198:

1172:

1138:

1104:

1063:

1036:

1028:

1000:

953:

868:

864:

863:

845:

785:

781:

780:

762:

693:

659:

655:

654:

633:

627:

588:

577:

557:

545:

516:

511:

507:

506:

497:

476:

472:

471:

462:

442:

389:

376:

363:

357:

318:

312:

291:

287:

286:

268:

242:

216:

177:

164:

147:

127:

107:

59:Learn how and when to remove this message

43:, without removing the technical details.

79:which models the possible trades in the

1247:

1272:

1261:

1253:

1251:

1226:{\displaystyle K=\mathbb {R} _{+}^{d}}

1292:SIAM Journal on Financial Mathematics

540:A process of (random) solvency cones

41:make it understandable to non-experts

7:

457:is any closed convex cone such that

1049:{\displaystyle t<{\frac {1}{2}}}

345:{\displaystyle e^{i},1\leq i\leq m}

668:

276:

149:

109:

14:

1133:therefore there is arbitrage if

1023:therefore there is arbitrage if

20:

1120:

1101:

1098:

1095:

1083:

1080:

1077:

1065:

1010:

991:

988:

985:

973:

970:

967:

955:

916:

904:

889:

877:

806:

794:

569:

563:

279:

273:

1:

1329:Discrete Applied Mathematics

87:. Specifically, it is the

1403:

1058:someone offers tM for 1A:

948:someone offers 1A for tM:

263:), then the solvency cone

1351:10.1016/j.dam.2015.01.030

719:consistent pricing system

613:self-financing portfolios

1387:Financial risk modeling

230:{\displaystyle m\leq d}

1271:Cite journal requires

1227:

1181:

1153:

1152:{\displaystyle t>2}

1127:

1050:

1017:

935:

835:With transaction costs

825:

742:

734:

711:

622:of the solvency cone (

598:

526:

486:

451:

423:

346:

301:

257:

231:

205:

136:

116:

1228:

1182:

1154:

1128:

1051:

1018:

936:

826:

740:

732:

712:

599:

527:

487:

452:

424:

347:

302:

258:

232:

206:

137:

117:

77:financial mathematics

75:is a concept used in

1197:

1171:

1137:

1062:

1027:

952:

844:

761:

626:

544:

496:

461:

441:

356:

311:

267:

241:

215:

146:

126:

115:{\displaystyle \Pi }

106:

1222:

1167:If a solvency cone

755:frictionless market

749:Frictionless market

593:

521:

256:{\displaystyle m=d}

1223:

1206:

1177:

1149:

1123:

1046:

1013:

931:

821:

743:

735:

707:

594:

547:

522:

505:

482:

447:

419:

342:

297:

253:

227:

201:

132:

112:

95:Mathematical basis

1314:10.1137/080743494

1180:{\displaystyle K}

1112:

1044:

1008:

450:{\displaystyle K}

142:assets such that

135:{\displaystyle d}

85:transaction costs

69:

68:

61:

1394:

1371:

1370:

1344:

1324:

1318:

1317:

1307:

1287:

1281:

1280:

1274:

1269:

1267:

1259:

1255:

1232:

1230:

1229:

1224:

1221:

1216:

1211:

1186:

1184:

1183:

1178:

1158:

1156:

1155:

1150:

1132:

1130:

1129:

1124:

1113:

1105:

1055:

1053:

1052:

1047:

1045:

1037:

1022:

1020:

1019:

1014:

1009:

1001:

940:

938:

937:

932:

873:

872:

867:

830:

828:

827:

822:

790:

789:

784:

716:

714:

713:

708:

706:

702:

698:

697:

664:

663:

658:

638:

637:

603:

601:

600:

595:

592:

587:

576:

572:

562:

561:

531:

529:

528:

523:

520:

515:

510:

491:

489:

488:

483:

481:

480:

475:

456:

454:

453:

448:

437:A solvency cone

428:

426:

425:

420:

394:

393:

381:

380:

371:

370:

352:and the vectors

351:

349:

348:

343:

323:

322:

306:

304:

303:

298:

296:

295:

290:

262:

260:

259:

254:

236:

234:

233:

228:

210:

208:

207:

202:

200:

199:

176:

172:

171:

141:

139:

138:

133:

121:

119:

118:

113:

81:financial market

64:

57:

53:

50:

44:

24:

23:

16:

1402:

1401:

1397:

1396:

1395:

1393:

1392:

1391:

1377:

1376:

1375:

1374:

1326:

1325:

1321:

1305:10.1.1.514.8477

1289:

1288:

1284:

1270:

1260:

1257:

1256:

1249:

1244:

1195:

1194:

1169:

1168:

1165:

1135:

1134:

1060:

1059:

1025:

1024:

950:

949:

862:

842:

841:

837:

779:

759:

758:

751:

727:

689:

653:

646:

642:

629:

624:

623:

553:

552:

548:

542:

541:

538:

494:

493:

470:

459:

458:

439:

438:

435:

385:

372:

359:

354:

353:

314:

309:

308:

285:

265:

264:

239:

238:

213:

212:

160:

156:

155:

144:

143:

124:

123:

104:

103:

97:

65:

54:

48:

45:

37:help improve it

34:

25:

21:

12:

11:

5:

1400:

1398:

1390:

1389:

1379:

1378:

1373:

1372:

1319:

1282:

1273:|journal=

1246:

1245:

1243:

1240:

1239:

1238:

1220:

1215:

1210:

1205:

1202:

1192:

1176:

1164:

1161:

1160:

1159:

1148:

1145:

1142:

1122:

1119:

1116:

1111:

1108:

1103:

1100:

1097:

1094:

1091:

1088:

1085:

1082:

1079:

1076:

1073:

1070:

1067:

1056:

1043:

1040:

1035:

1032:

1012:

1007:

1004:

999:

996:

993:

990:

987:

984:

981:

978:

975:

972:

969:

966:

963:

960:

957:

930:

927:

924:

921:

918:

915:

912:

909:

906:

903:

900:

897:

894:

891:

888:

885:

882:

879:

876:

871:

866:

861:

858:

855:

852:

849:

836:

833:

820:

817:

814:

811:

808:

805:

802:

799:

796:

793:

788:

783:

778:

775:

772:

769:

766:

750:

747:

726:

723:

705:

701:

696:

692:

688:

685:

682:

679:

676:

673:

670:

667:

662:

657:

652:

649:

645:

641:

636:

632:

606:market process

591:

586:

583:

580:

575:

571:

568:

565:

560:

556:

551:

537:

534:

519:

514:

509:

504:

501:

479:

474:

469:

466:

446:

434:

431:

418:

415:

412:

409:

406:

403:

400:

397:

392:

388:

384:

379:

375:

369:

366:

362:

341:

338:

335:

332:

329:

326:

321:

317:

294:

289:

284:

281:

278:

275:

272:

252:

249:

246:

226:

223:

220:

198:

195:

192:

189:

186:

183:

180:

175:

170:

167:

163:

159:

154:

151:

131:

111:

101:bid-ask matrix

96:

93:

67:

66:

28:

26:

19:

13:

10:

9:

6:

4:

3:

2:

1399:

1388:

1385:

1384:

1382:

1368:

1364:

1360:

1356:

1352:

1348:

1343:

1338:

1334:

1330:

1323:

1320:

1315:

1311:

1306:

1301:

1297:

1293:

1286:

1283:

1278:

1265:

1254:

1252:

1248:

1241:

1236:

1218:

1213:

1203:

1200:

1193:

1190:

1189:

1188:

1174:

1162:

1146:

1143:

1140:

1117:

1114:

1109:

1106:

1092:

1089:

1086:

1074:

1071:

1068:

1057:

1041:

1038:

1033:

1030:

1005:

1002:

997:

994:

982:

979:

976:

964:

961:

958:

947:

946:

945:

942:

925:

922:

919:

913:

910:

907:

901:

898:

895:

892:

886:

883:

880:

874:

869:

859:

856:

850:

847:

834:

832:

815:

812:

809:

803:

800:

797:

791:

786:

776:

773:

767:

764:

756:

748:

746:

739:

731:

724:

722:

720:

703:

699:

694:

690:

686:

683:

680:

677:

674:

671:

665:

660:

650:

647:

643:

639:

634:

630:

621:

616:

614:

609:

607:

589:

584:

581:

578:

573:

566:

558:

554:

549:

535:

533:

517:

512:

502:

499:

477:

467:

464:

444:

432:

430:

416:

413:

410:

407:

404:

401:

398:

395:

390:

386:

382:

377:

373:

367:

364:

360:

339:

336:

333:

330:

327:

324:

319:

315:

292:

282:

270:

250:

247:

244:

224:

221:

218:

196:

193:

190:

187:

184:

181:

178:

173:

168:

165:

161:

157:

152:

129:

102:

94:

92:

90:

86:

82:

78:

74:

73:solvency cone

63:

60:

52:

49:December 2013

42:

38:

32:

29:This article

27:

18:

17:

1332:

1328:

1322:

1298:(1): 66–95.

1295:

1291:

1285:

1264:cite journal

1166:

943:

838:

752:

744:

617:

610:

605:

539:

436:

98:

72:

70:

55:

46:

30:

1335:: 176–185.

99:If given a

89:convex cone

1242:References

1163:Properties

433:Definition

1359:0166-218X

1342:1402.2221

1300:CiteSeerX

1099:→

1081:→

989:→

971:→

923:≥

896:≥

860:∈

813:≥

777:∈

687:≤

675:∈

669:∀

651:∈

620:dual cone

567:ω

503:⊇

468:⊆

414:≤

402:≤

383:−

361:π

337:≤

331:≤

283:⊂

277:Π

222:≤

194:≤

182:≤

162:π

150:Π

110:Π

1381:Category

1367:12427504

1235:illiquid

725:Examples

35:Please

1365:

1357:

1302:

1363:S2CID

1337:arXiv

753:In a

1355:ISSN

1277:help

1144:>

1034:<

618:The

536:Uses

492:and

211:and

122:for

71:The

1347:doi

1333:186

1310:doi

39:to

1383::

1361:.

1353:.

1345:.

1331:.

1308:.

1294:.

1268::

1266:}}

1262:{{

1250:^

1187::

941:.

721:.

615:.

608:.

532:.

429:.

1369:.

1349::

1339::

1316:.

1312::

1296:1

1279:)

1275:(

1237:.

1219:d

1214:+

1209:R

1204:=

1201:K

1175:K

1147:2

1141:t

1121:)

1118:0

1115:,

1110:2

1107:t

1102:(

1096:)

1093:t

1090:,

1087:0

1084:(

1078:)

1075:0

1072:,

1069:1

1066:(

1042:2

1039:1

1031:t

1011:)

1006:2

1003:1

998:,

995:0

992:(

986:)

983:0

980:,

977:1

974:(

968:)

965:t

962:,

959:0

956:(

929:}

926:0

920:x

917:)

914:2

911:,

908:1

905:(

902:,

899:0

893:x

890:)

887:1

884:,

881:2

878:(

875::

870:2

865:R

857:x

854:{

851:=

848:K

819:}

816:0

810:x

807:)

804:1

801:,

798:1

795:(

792::

787:2

782:R

774:x

771:{

768:=

765:K

704:}

700:v

695:T

691:w

684:0

681::

678:K

672:v

666::

661:d

656:R

648:w

644:{

640:=

635:+

631:K

590:T

585:0

582:=

579:t

574:}

570:)

564:(

559:t

555:K

550:{

518:d

513:+

508:R

500:K

478:d

473:R

465:K

445:K

417:d

411:j

408:,

405:i

399:1

396:,

391:j

387:e

378:i

374:e

368:j

365:i

340:m

334:i

328:1

325:,

320:i

316:e

293:d

288:R

280:)

274:(

271:K

251:d

248:=

245:m

225:d

219:m

197:d

191:j

188:,

185:i

179:1

174:)

169:j

166:i

158:(

153:=

130:d

62:)

56:(

51:)

47:(

33:.

Text is available under the Creative Commons Attribution-ShareAlike License. Additional terms may apply.