95:, BaaS aims at integrating as many service providers as needed into one comprehensive process to complete a financial service in an effective and timely manner. It is implied that a BaaS would include certain features in addition to providing a financial service. There must be means for managing, deploying and delivery of the services' environment. The services must of course be in legal compliance with the banking laws in the regions where it is made available, with (at least) one entity within the process possessing a banking license. Of utmost importance is the assurance that proper mechanisms are in place to provide security, such as strong authentication and additional measures to protect sensitive information from unauthorized access throughout the entire process. These security mechanisms must be in compliance with laws of data protection for the jurisdictions involved. With the proliferation and acceptance of BaaS, the emergence and rapid growth of

61:

108:

229:

As such, this presents a challenge to a satisfactory user experience if the user needs to constantly be authenticated while performing an online transaction across several domains or applications. Instead, the many domains and apps that are used need to be interwoven in such a way that once a user has been authenticated, this authentication will carry through as he conducts his transaction. This can be accomplished through the 3 degrees of freedom in

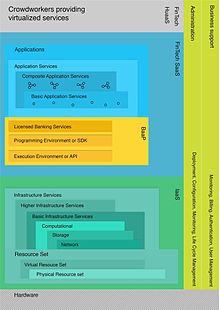

178:(software as a service) refers to all atomic or composite software-based financial services that are available on-demand. When these services are provided through a BaaP, they will need to be compliant with the BaaP's API specifications. The services may either be physically deployed in the BaaP's domain or work externally. This gives the potential for the ability to plug financial services from other banks into the BaaP to create new

354:

1900:

22:

124:

without having to build all the products that would be needed. The API-based bank as a service platform serves as the back-end that hosts standalone independent fintech startups and integrates seamlessly with any existing back-office of traditional banks. This allows non-banks to easily and cost-effectively launch additional financial products and expand into additional markets.

204:

including user authentication and other features. The bank would appear as any other online bank where all banking services are presented and seamlessly integrated in a single user interface. Another option is that the bank will operate as a white label bank, which will then have a software as a service provider on top of the BaaP operating as the front-end to the end-customer.

228:

remains a constant and serious threat to the banking industry. The introduction of additional entrance gateways by offering increased amounts of composite online services does increase the risk for cyber-crime. It is important that each service be properly firewalled to prevent malicious intrusions.

132:

Dynamic development and growth in the world of fintech have made the API-based bank-as-a-service stack obsolete in contexts where tech-companies now own licenses to operate as regulated banks, thus eliminating the reliance on classic banks. Embracing the new developments in financial technology and

123:

With this technology, based on the BaaS-platform, it is possible to create fintech banks, which could improve banking processes and provide increased convenience for banking clients. In such a constellation, fintech banks are enabled to compete directly with banks by offering core-banking services

165:

At the top of the IaaS model would be banking as a platform provider (BaaP). The BaaP would be a bank that is fully licensed or use an external regulated bank's licensed banking services. The decomposed banking services (fintech SaaS) are in essence, plugged into this layer. Data-security plays a

216:

A single service provider is at a greater risk of failure than a provider that offers a larger portfolio of services. Using an integrated BaaS structure efficiently provides an end-to-end value proposition that frees the service provider from having to develop all the needed peripheral services,

194:

Humans as a service represents the top layer of the proposed revision of the BaaS stack. While at the onset this layer may not seem especially important, as fintech services continue to grow as a segment in the financial service market, services performed by cloudworkers will take on increased

203:

The consequence of having a decomposed stack is that there are multiple ways that the customer's front-end could be presented. One way would allow the BaaP provider to appear directly as a bank to its customers. This necessitates the provision of a front-end user interface to the end-customers

313:

Fintechs in Africa have provided an original financing solution in a previously unserved and untapped banking market. Because it is primarily mobile-based, Africa fintech is subject to national jurisdiction in regards to regulating financial markets and mobile telecommunications.

207:

White label banking can be an answer to the challenge platform providers face in attaining customers. It can be used to offer banking services in environments where a large group of users already exist, including chains of grocery stores, hypermarkets or existing online portals.

304:

Asia has a strong disadvantage because of its high fragmentation of jurisdiction areas compared to Europe. Fintechs can plug into the national banking-as-a-service hub to provide their specific regulated and licensed face to their customers.

671:"Commission Directive implementing Directive 2004/39/EC of the European Parliament and of the Council as regards organisational requirements and operating conditions for investment firms, and defined terms for the purposes of that Directive"

625:"Directive 2013/36/EU on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms, amending Directive 2002/87/EC and repealing Directives 2006/48/EC and 2006/49/EC"

1418:

115:

Skinner suggested a 3-layer representation of the BaaS stack. In this stack, the underlying infrastructure-as-a-service is provided by a traditional, licensed and regulated bank. Above this bank would be the centralized

1527:

284:

for electronic transactions throughout the entire end-to-end process. Additional oversight for financial and insurance transactions are provided through

Directive 2004/39/EC and Directive 2016/97/EU.

120:

layer that

Skinner refers to as "bank as a service". Added on to the bank as a service is a group of decomposed banking services consisting of an ecosystem of fintech startups and service providers.

602:"Directive (EU) 2015/2366 on payment services in the internal market, amending Directives 2002/65/EC, 2009/110/EC and 2013/36/EU and Regulation (EU) No 1093/2010, and repealing Directive 2007/64/EC"

769:

1522:

145:(IaaS) layer provides basic infrastructure services through an IaaS provider. A majority of these services would be available on demand and do not necessarily need to be fintech services (like

268:) that was adopted in November 2015. Banking licenses are overseen by competent national authorities in accordance to Directive 2013/36/EU and Article 14 of Regulation (EU) No 1024/2013. The

1572:

330:

In Brazil, BaaS is regulated by the

Brazilian Central Bank within the rules of a Payment Institution. The best known BaaS' fintechs providers in Brazil are Matera, Zoop, Dock, and

166:

crucial role in the BaaP. There is a need for monitoring functions that will enable seamless and secure operations across applications and domains through secure authentication.

1587:

1468:

742:

186:

services. This does, however, present a challenge in verifying that none of the plugged-in services will violate regulations that have been imposed by banking authorities.

1799:

1507:

1764:

1703:

1592:

217:

including authentication and other security services. Those who adopt the BaaS structure are able to provide a higher level of trust than a smaller provider might do.

491:

Lenk, Alexander; Klems, Markus; Nimis, Jens; Tai, Stefan; Sandholm, Thomas (May 23, 2009). "What's inside the Cloud? An architectural map of the Cloud landscape".

1458:

1537:

195:

importance. This is a behind the scenes component that end-users will be unable to discern between a complete automated service and one that includes HuaaS.

1547:

1463:

1453:

1779:

1304:

971:

508:

1408:

1602:

1759:

1567:

1557:

1517:

670:

1499:

1473:

1433:

561:

293:

99:

can be expected. Fintech is “a business that aims at providing financial services by making use of software and modern technology.”

1676:

1597:

1582:

1478:

1342:

835:

746:

719:

578:

1365:

1552:

1483:

1448:

1204:

1774:

1754:

1708:

1671:

1577:

1532:

1244:

891:

1681:

1512:

1487:

1274:

1542:

624:

1929:

1562:

601:

142:

111:

This stack can be used with a licensed bank as foundation, a BaaS as middleware, and an ecosystems of FinTechs on top.

1924:

1179:

956:

261:

413:

1794:

1738:

1718:

1443:

1403:

941:

322:

Australia's government is behind in regulating fintech in comparison to the

European Payment Services Directive.

277:

252:

Banking is a highly regulated industry throughout the world and online banks utilizing BaaS are no exception.

1789:

1784:

1656:

1438:

1830:

1428:

1423:

1370:

1154:

856:

281:

1934:

1809:

1380:

1335:

1149:

1134:

1071:

1031:

1021:

961:

921:

828:

696:

183:

179:

60:

1628:

1413:

1214:

1169:

1089:

1083:

1056:

1036:

981:

976:

896:

802:

647:

182:

services. The result is that traditional banking services can now be virtualized and dispatched via

1845:

1713:

1698:

1648:

1385:

1279:

1249:

1229:

1139:

1099:

1026:

1016:

1011:

372:

146:

790:

107:

1885:

1264:

1259:

1144:

1119:

1066:

991:

906:

526:

514:

1855:

1638:

1194:

1051:

996:

926:

911:

871:

557:

504:

342:

Russian banks are actively introducing BaaS, for example, the largest private bank Alfa Bank.

40:

34:

1903:

1769:

1728:

1666:

1618:

1375:

1328:

1189:

1159:

1129:

1124:

1104:

1076:

1041:

966:

876:

821:

496:

331:

292:

In the United States, banks are highly regulated at both the state and federal levels. The

64:"Banking as a service" stack based on the cloud stack by Scholten, derived from Lenk et al.

1633:

1623:

1294:

1289:

1209:

1114:

1094:

1006:

1001:

931:

916:

538:

230:

133:

services, the banking-as-a-service stack can be redefined in analogy to the cloud stack.

1870:

1850:

1723:

1284:

1269:

1234:

1219:

1199:

1061:

1046:

886:

861:

377:

359:

273:

154:

76:

21:

1918:

1840:

1835:

1733:

1693:

1688:

1309:

951:

936:

901:

92:

518:

1880:

1661:

1184:

1109:

435:

387:

382:

367:

1875:

1395:

1299:

1239:

1224:

1174:

1164:

866:

225:

500:

1860:

946:

349:

117:

79:(such as current accounts and credit cards) to non-bank third parties through

1825:

463:

813:

881:

493:

2009 ICSE Workshop on

Software Engineering Challenges of Cloud Computing

1351:

986:

845:

96:

153:). This layer would include the server and communication hardware (

1865:

1254:

269:

106:

59:

1804:

265:

175:

1324:

817:

556:. Singapore: Marshall Cavendish International (Asia) Pte Ltd.

150:

80:

15:

43:

it by defining technical terminology, and by adding examples.

770:"Australia needs to foster FinTech with level playing field"

697:"Directive (EU) 2016/97 on insurance distribution (recast)"

554:

Digital Bank: Strategies to Launch or Become a

Digital Bank

1320:

579:"Digital Authentication: Factors, Mechanisms and Schemes"

212:

Integrated BaaS structure vs. single service offering

1818:

1747:

1647:

1611:

1498:

1394:

1358:

464:"Overview of APIs and Bank-as-a-Service in FinTech"

1800:International Association of Privacy Professionals

743:"Five factors that differentiate Africa's fintech"

296:(SEC) is responsible for much of this regulation.

1765:Computer Professionals for Social Responsibility

486:

484:

260:In Europe, BaaS for fintechs is overseen by the

29:This article may be written in a style that is

457:

455:

453:

414:"Banking-as-a-Service - what you need to know"

1336:

829:

8:

720:"A wave of regulation is coming for fintech"

1343:

1329:

1321:

836:

822:

814:

407:

405:

403:

695:The European Parliament and the Council.

623:The European Parliament and the Council.

600:The European Parliament and the Council.

264:(PSD, 2007/64/EC) and its 2nd amendment (

669:Commission of the European Communities.

627:. Official Journal of the European Union

604:. Official Journal of the European Union

399:

534:

524:

1780:Electronic Privacy Information Center

1305:Valuation using discounted cash flows

272:regulation provides requirements for

7:

552:Skinner, Chris (September 7, 2014).

1760:Center for Democracy and Technology

294:Securities and Exchange Commission

237:Identity federation across domains

137:Infrastructure as a service (IaaS)

14:

793:O que é instituição de pagamento?

1899:

1898:

1366:Right of access to personal data

806:Banco BV’s Investment in S3 Bank

772:. The Australian Business Review

352:

240:Identity propagation across apps

33:to be readily understandable by

20:

1205:Quantitative behavioral finance

1775:Electronic Frontier Foundation

1755:American Civil Liberties Union

1709:Privacy-enhancing technologies

1245:Strategic financial management

892:Bull (stock market speculator)

1:

1275:Sustainable Development Goals

745:. CNBCAFRICA. Archived from

161:Banking as a platform (BaaP)

1500:Data protection authorities

143:infrastructure as a service

1951:

1704:Social networking services

957:Enterprise risk management

718:Marino, Jon (6 May 2016).

501:10.1109/CLOUD.2009.5071529

262:Payment Services Directive

1894:

1795:Global Network Initiative

1739:Virtual assistant privacy

1719:Privacy-invasive software

942:Diversification (finance)

852:

803:globallegalchronicle.com/

278:electronic identification

243:Level of authentication

1790:Future of Privacy Forum

1785:European Digital Rights

1831:Cellphone surveillance

1748:Advocacy organizations

1371:Expectation of privacy

1155:Investment performance

857:Alternative investment

112:

75:) is the provision of

65:

1810:Privacy International

1381:Right to be forgotten

1150:Investment management

1135:International finance

962:Environmental finance

922:Computational finance

676:. European Commission

648:"Understanding eIDAS"

199:Potential consequence

184:composite application

180:composite application

110:

63:

1215:Risk-return spectrum

1170:Mathematical finance

1090:Fundamental analysis

1084:Financial technology

982:Experimental finance

977:Exchange traded fund

469:. ASAP Agency Moscow

436:"FinTech Definition"

69:Banking as a service

1846:Global surveillance

1714:Privacy engineering

1699:Personal identifier

1649:Information privacy

1386:Post-mortem privacy

1280:Sustainable finance

1250:Statistical finance

1230:Statistical finance

1140:Investment advisory

1100:Greater fool theory

741:van der Beek, Wim.

373:Account aggregation

147:Amazon Web Services

1930:Banking technology

1886:Personality rights

1265:Structured product

1260:Structured finance

1145:Investment banking

1120:History of banking

907:Capital management

749:on 18 January 2017

495:. pp. 23–31.

412:Scholten, Ulrich.

113:

66:

1925:Financial markets

1912:

1911:

1856:Mass surveillance

1318:

1317:

1195:Position of trust

927:Corporate finance

912:Capital structure

872:Asset (economics)

844:General areas of

510:978-1-4244-3713-9

128:Cloud-based stack

58:

57:

35:general audiences

1942:

1902:

1901:

1770:Data Privacy Lab

1729:Privacy software

1376:Right to privacy

1345:

1338:

1331:

1322:

1190:Personal finance

1180:Over-the-counter

1160:Investor profile

1130:Impact investing

1125:History of money

1105:Growth investing

967:Equity (finance)

877:Asset allocation

838:

831:

824:

815:

808:

800:

794:

788:

782:

781:

779:

777:

765:

759:

758:

756:

754:

738:

732:

731:

729:

727:

715:

709:

708:

706:

704:

692:

686:

685:

683:

681:

675:

666:

660:

659:

657:

655:

646:Turner, Dawn M.

643:

637:

636:

634:

632:

620:

614:

613:

611:

609:

597:

591:

590:

588:

586:

574:

568:

567:

549:

543:

542:

536:

532:

530:

522:

488:

479:

478:

476:

474:

468:

462:Skinner, Chris.

459:

448:

447:

445:

443:

438:. FinTech Weekly

432:

426:

425:

423:

421:

409:

362:

357:

356:

355:

77:banking products

53:

50:

44:

24:

16:

1950:

1949:

1945:

1944:

1943:

1941:

1940:

1939:

1915:

1914:

1913:

1908:

1890:

1814:

1743:

1643:

1607:

1494:

1488:amended in 2020

1390:

1354:

1349:

1319:

1314:

1295:Too big to fail

1290:Systematic risk

1210:Quantum finance

1115:Hedge (finance)

1095:Government bond

932:Cost of capital

917:Climate finance

848:

842:

812:

811:

801:

797:

789:

785:

775:

773:

768:Lucas, George.

767:

766:

762:

752:

750:

740:

739:

735:

725:

723:

717:

716:

712:

702:

700:

694:

693:

689:

679:

677:

673:

668:

667:

663:

653:

651:

645:

644:

640:

630:

628:

622:

621:

617:

607:

605:

599:

598:

594:

584:

582:

576:

575:

571:

564:

551:

550:

546:

533:

523:

511:

490:

489:

482:

472:

470:

466:

461:

460:

451:

441:

439:

434:

433:

429:

419:

417:

411:

410:

401:

396:

358:

353:

351:

348:

340:

328:

320:

311:

302:

290:

258:

250:

231:digital banking

223:

214:

201:

192:

172:

163:

139:

130:

105:

103:API-based stack

89:

54:

48:

45:

38:

25:

12:

11:

5:

1948:

1946:

1938:

1937:

1932:

1927:

1917:

1916:

1910:

1909:

1907:

1906:

1895:

1892:

1891:

1889:

1888:

1883:

1878:

1873:

1871:Search warrant

1868:

1863:

1858:

1853:

1851:Identity theft

1848:

1843:

1838:

1833:

1828:

1822:

1820:

1816:

1815:

1813:

1812:

1807:

1802:

1797:

1792:

1787:

1782:

1777:

1772:

1767:

1762:

1757:

1751:

1749:

1745:

1744:

1742:

1741:

1736:

1731:

1726:

1724:Privacy policy

1721:

1716:

1711:

1706:

1701:

1696:

1691:

1686:

1685:

1684:

1679:

1674:

1664:

1659:

1653:

1651:

1645:

1644:

1642:

1641:

1636:

1631:

1626:

1621:

1615:

1613:

1609:

1608:

1606:

1605:

1603:United Kingdom

1600:

1595:

1590:

1585:

1580:

1575:

1570:

1565:

1560:

1555:

1550:

1545:

1540:

1535:

1530:

1525:

1520:

1518:European Union

1515:

1510:

1504:

1502:

1496:

1495:

1493:

1492:

1491:

1490:

1476:

1474:United Kingdom

1471:

1466:

1461:

1456:

1451:

1446:

1441:

1436:

1434:European Union

1431:

1426:

1421:

1416:

1411:

1406:

1400:

1398:

1392:

1391:

1389:

1388:

1383:

1378:

1373:

1368:

1362:

1360:

1356:

1355:

1350:

1348:

1347:

1340:

1333:

1325:

1316:

1315:

1313:

1312:

1307:

1302:

1297:

1292:

1287:

1285:Swap (finance)

1282:

1277:

1272:

1270:Sustainability

1267:

1262:

1257:

1252:

1247:

1242:

1237:

1235:Stock exchange

1232:

1227:

1222:

1220:Social finance

1217:

1212:

1207:

1202:

1200:Public finance

1197:

1192:

1187:

1182:

1177:

1172:

1167:

1162:

1157:

1152:

1147:

1142:

1137:

1132:

1127:

1122:

1117:

1112:

1107:

1102:

1097:

1092:

1087:

1081:

1080:

1079:

1074:

1069:

1064:

1059:

1054:

1049:

1044:

1039:

1034:

1029:

1024:

1019:

1014:

1009:

1004:

999:

994:

984:

979:

974:

969:

964:

959:

954:

949:

944:

939:

934:

929:

924:

919:

914:

909:

904:

899:

894:

889:

887:Bond (finance)

884:

879:

874:

869:

864:

862:Angel investor

859:

853:

850:

849:

843:

841:

840:

833:

826:

818:

810:

809:

795:

783:

760:

733:

710:

687:

661:

650:. Cryptomathic

638:

615:

592:

581:. Cryptomathic

577:Balbas, Luis.

569:

563:978-9814516464

562:

544:

535:|journal=

509:

480:

449:

427:

416:. VentureSkies

398:

397:

395:

392:

391:

390:

385:

380:

378:Online banking

375:

370:

364:

363:

360:Banking portal

347:

344:

339:

336:

327:

324:

319:

316:

310:

307:

301:

298:

289:

286:

282:trust services

274:authentication

257:

254:

249:

246:

245:

244:

241:

238:

222:

219:

213:

210:

200:

197:

191:

188:

171:

168:

162:

159:

155:physical layer

138:

135:

129:

126:

104:

101:

88:

85:

56:

55:

28:

26:

19:

13:

10:

9:

6:

4:

3:

2:

1947:

1936:

1933:

1931:

1928:

1926:

1923:

1922:

1920:

1905:

1897:

1896:

1893:

1887:

1884:

1882:

1879:

1877:

1874:

1872:

1869:

1867:

1864:

1862:

1859:

1857:

1854:

1852:

1849:

1847:

1844:

1842:

1841:Eavesdropping

1839:

1837:

1836:Data security

1834:

1832:

1829:

1827:

1824:

1823:

1821:

1817:

1811:

1808:

1806:

1803:

1801:

1798:

1796:

1793:

1791:

1788:

1786:

1783:

1781:

1778:

1776:

1773:

1771:

1768:

1766:

1763:

1761:

1758:

1756:

1753:

1752:

1750:

1746:

1740:

1737:

1735:

1734:Secret ballot

1732:

1730:

1727:

1725:

1722:

1720:

1717:

1715:

1712:

1710:

1707:

1705:

1702:

1700:

1697:

1695:

1694:Personal data

1692:

1690:

1687:

1683:

1680:

1678:

1675:

1673:

1670:

1669:

1668:

1665:

1663:

1660:

1658:

1655:

1654:

1652:

1650:

1646:

1640:

1637:

1635:

1632:

1630:

1627:

1625:

1622:

1620:

1617:

1616:

1614:

1610:

1604:

1601:

1599:

1596:

1594:

1591:

1589:

1586:

1584:

1581:

1579:

1576:

1574:

1571:

1569:

1566:

1564:

1561:

1559:

1556:

1554:

1551:

1549:

1546:

1544:

1541:

1539:

1536:

1534:

1531:

1529:

1526:

1524:

1521:

1519:

1516:

1514:

1511:

1509:

1506:

1505:

1503:

1501:

1497:

1489:

1485:

1482:

1481:

1480:

1479:United States

1477:

1475:

1472:

1470:

1467:

1465:

1462:

1460:

1457:

1455:

1452:

1450:

1447:

1445:

1442:

1440:

1437:

1435:

1432:

1430:

1427:

1425:

1422:

1420:

1417:

1415:

1412:

1410:

1407:

1405:

1402:

1401:

1399:

1397:

1393:

1387:

1384:

1382:

1379:

1377:

1374:

1372:

1369:

1367:

1364:

1363:

1361:

1357:

1353:

1346:

1341:

1339:

1334:

1332:

1327:

1326:

1323:

1311:

1310:Watered stock

1308:

1306:

1303:

1301:

1298:

1296:

1293:

1291:

1288:

1286:

1283:

1281:

1278:

1276:

1273:

1271:

1268:

1266:

1263:

1261:

1258:

1256:

1253:

1251:

1248:

1246:

1243:

1241:

1238:

1236:

1233:

1231:

1228:

1226:

1223:

1221:

1218:

1216:

1213:

1211:

1208:

1206:

1203:

1201:

1198:

1196:

1193:

1191:

1188:

1186:

1183:

1181:

1178:

1176:

1173:

1171:

1168:

1166:

1163:

1161:

1158:

1156:

1153:

1151:

1148:

1146:

1143:

1141:

1138:

1136:

1133:

1131:

1128:

1126:

1123:

1121:

1118:

1116:

1113:

1111:

1108:

1106:

1103:

1101:

1098:

1096:

1093:

1091:

1088:

1085:

1082:

1078:

1075:

1073:

1070:

1068:

1065:

1063:

1060:

1058:

1055:

1053:

1050:

1048:

1045:

1043:

1040:

1038:

1035:

1033:

1030:

1028:

1025:

1023:

1020:

1018:

1015:

1013:

1010:

1008:

1005:

1003:

1000:

998:

995:

993:

990:

989:

988:

985:

983:

980:

978:

975:

973:

970:

968:

965:

963:

960:

958:

955:

953:

952:Eco-investing

950:

948:

945:

943:

940:

938:

937:Disinvestment

935:

933:

930:

928:

925:

923:

920:

918:

915:

913:

910:

908:

905:

903:

902:Capital asset

900:

898:

895:

893:

890:

888:

885:

883:

880:

878:

875:

873:

870:

868:

865:

863:

860:

858:

855:

854:

851:

847:

839:

834:

832:

827:

825:

820:

819:

816:

807:

804:

799:

796:

792:

787:

784:

771:

764:

761:

748:

744:

737:

734:

721:

714:

711:

698:

691:

688:

672:

665:

662:

649:

642:

639:

626:

619:

616:

603:

596:

593:

580:

573:

570:

565:

559:

555:

548:

545:

540:

528:

520:

516:

512:

506:

502:

498:

494:

487:

485:

481:

465:

458:

456:

454:

450:

437:

431:

428:

415:

408:

406:

404:

400:

393:

389:

386:

384:

381:

379:

376:

374:

371:

369:

366:

365:

361:

350:

345:

343:

337:

335:

333:

325:

323:

317:

315:

308:

306:

299:

297:

295:

288:United States

287:

285:

283:

279:

275:

271:

267:

263:

255:

253:

247:

242:

239:

236:

235:

234:

233:, involving:

232:

227:

220:

218:

211:

209:

205:

198:

196:

189:

187:

185:

181:

177:

169:

167:

160:

158:

156:

152:

148:

144:

136:

134:

127:

125:

121:

119:

109:

102:

100:

98:

94:

93:value network

86:

84:

82:

78:

74:

70:

62:

52:

42:

36:

32:

27:

23:

18:

17:

1935:As a service

1881:Human rights

1396:Privacy laws

1185:Pension fund

1110:Growth stock

1032:institutions

897:Asset growth

805:

798:

786:

774:. Retrieved

763:

751:. Retrieved

747:the original

736:

724:. Retrieved

713:

701:. Retrieved

690:

678:. Retrieved

664:

652:. Retrieved

641:

629:. Retrieved

618:

606:. Retrieved

595:

583:. Retrieved

572:

553:

547:

492:

471:. Retrieved

440:. Retrieved

430:

418:. Retrieved

388:Open Finance

383:Open banking

368:as a service

341:

329:

321:

312:

303:

291:

259:

251:

224:

215:

206:

202:

193:

173:

170:FinTech SaaS

164:

140:

131:

122:

114:

90:

72:

68:

67:

49:January 2018

46:

31:too abstract

30:

1876:Wiretapping

1588:Switzerland

1573:South Korea

1563:Philippines

1553:Netherlands

1548:Isle of Man

1469:Switzerland

1449:New Zealand

1300:Toxic asset

1240:Stockbroker

1225:Speculation

1175:Mutual fund

1165:Market risk

1072:social work

1022:engineering

867:Super angel

791:bcb.gov.br/

420:25 December

248:Regulations

226:Cyber-crime

87:Description

1919:Categories

1861:Panopticon

1484:California

1359:Principles

1057:regulation

1037:management

947:Divestment

776:17 January

753:17 January

726:17 January

703:17 January

680:17 January

654:17 January

631:17 January

608:17 January

585:17 January

473:16 January

442:16 January

394:References

118:middleware

1826:Anonymity

1662:Financial

1639:Workplace

1629:Education

1538:Indonesia

1508:Australia

1464:Sri Lanka

1459:Singapore

1404:Australia

1086:(Fintech)

1027:inclusion

1017:economics

1012:deepening

987:Financial

699:. EUR-Lex

537:ignored (

527:cite book

318:Australia

1904:Category

1819:See also

1672:Facebook

1667:Internet

1619:Consumer

1593:Thailand

1067:services

992:analysis

882:Bad debt

519:14619005

346:See also

221:Security

174:Fintech

1682:Twitter

1634:Medical

1624:Digital

1543:Ireland

1528:Germany

1513:Denmark

1439:Germany

1429:England

1424:Denmark

1352:Privacy

1052:planner

997:analyst

846:finance

332:S3 Bank

97:fintech

41:improve

39:Please

1677:Google

1598:Turkey

1583:Sweden

1568:Poland

1558:Norway

1523:France

1454:Russia

1414:Canada

1409:Brazil

1077:system

1042:market

722:. CNBC

560:

517:

507:

338:Russia

326:Brazil

309:Africa

256:Europe

1866:PRISM

1689:Email

1612:Areas

1578:Spain

1533:India

1444:Ghana

1419:China

1255:Stock

1007:crime

1002:asset

674:(PDF)

515:S2CID

467:(PDF)

270:eIDAS

190:HuaaS

91:As a

1805:NOYB

1062:risk

1047:plan

778:2017

755:2017

728:2017

705:2017

682:2017

656:2017

633:2017

610:2017

587:2017

558:ISBN

539:help

505:ISBN

475:2017

444:2017

422:2016

300:Asia

280:and

276:and

266:PSD2

176:SaaS

141:The

81:APIs

73:BaaS

1657:Law

972:ESG

497:doi

157:).

151:OVH

149:or

1921::

1486:,

531::

529:}}

525:{{

513:.

503:.

483:^

452:^

402:^

334:.

83:.

1344:e

1337:t

1330:v

837:e

830:t

823:v

780:.

757:.

730:.

707:.

684:.

658:.

635:.

612:.

589:.

566:.

541:)

521:.

499::

477:.

446:.

424:.

71:(

51:)

47:(

37:.

Text is available under the Creative Commons Attribution-ShareAlike License. Additional terms may apply.